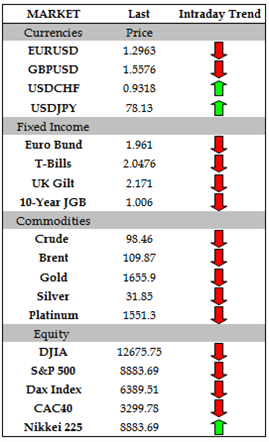

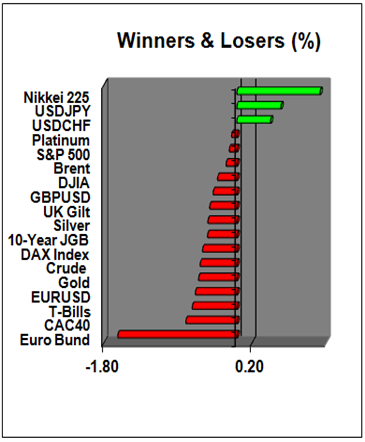

Investor optimism was dented yesterday after European finance ministers failed to agree on the Greek debt swap deal and called for a greater contribution from debt holders. Finance ministers are pushing bondholders for greater debt relief by asking them to accept lower interest returns in the proposed debt swap deal. The stalling of negotiations has fuelled concerns that Greece will fail to make a bond payment due in late March. The EUR fell from a high of 1.3065 during the Asian session yesterday to as low as 1.2948 in early European trade today.

In more sobering news, the IMF has cut global growth forecasts and warned that the "epicentre of the danger is Europe but the rest of the word is increasingly affected." It cut global growth for 2012 from a September forecast of 4 percent to 3.3 percent and predicted a recession in Europe. The IMF called for an increase in the eurozone's rescue fund and a more active role from the ECB to address the crisis. In a dire warning, the IMF warned of a 1930's style worldwide depression unless more countries play their part and identified a possible global financing need of over $1 trillion in the next few years. Inflation in the UK for December fell to its lowest level in 6 months at an annual rate of 4.2% and the economy contracted in the fourth quarter which saw the GBP fall to as low as 1.5528.

Yesterday, US equities fell after advancing for five consecutive sessions as negotiations stalled in the proposed Greek debt swap deal. Furthermore, the IMF warned that there was potential for "political paralysis" in the United States that could lead to an unwinding of stimulus spending. Asian markets there were opened today closed higher while European shares are down about 1% mid session, falling for the second day, as Ericsson and Novartis missed earnings estimates.

In more sobering news, the IMF has cut global growth forecasts and warned that the "epicentre of the danger is Europe but the rest of the word is increasingly affected." It cut global growth for 2012 from a September forecast of 4 percent to 3.3 percent and predicted a recession in Europe. The IMF called for an increase in the eurozone's rescue fund and a more active role from the ECB to address the crisis. In a dire warning, the IMF warned of a 1930's style worldwide depression unless more countries play their part and identified a possible global financing need of over $1 trillion in the next few years. Inflation in the UK for December fell to its lowest level in 6 months at an annual rate of 4.2% and the economy contracted in the fourth quarter which saw the GBP fall to as low as 1.5528.

Yesterday, US equities fell after advancing for five consecutive sessions as negotiations stalled in the proposed Greek debt swap deal. Furthermore, the IMF warned that there was potential for "political paralysis" in the United States that could lead to an unwinding of stimulus spending. Asian markets there were opened today closed higher while European shares are down about 1% mid session, falling for the second day, as Ericsson and Novartis missed earnings estimates.

FX News

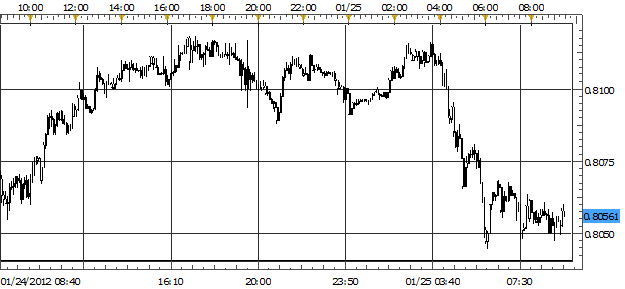

EUR/USD

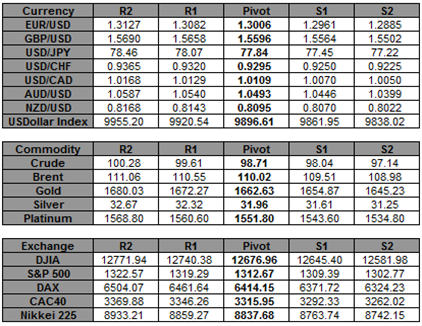

EUR/USD traded within a narrow range during Asian session (1.3014 - 1.3041) today perhaps due to the Lunar Year celebration. The same could be expected for the rest of the week for Asia if no surprises hit the market. At the time of writing, euro spiked up to 1.5050 as German IFO was released. Market was expecting 107.6 but actual came out as 108.3 (last 107.3). But the spike was very short-lived as it pulled back to the comfortable 1.3020 - 1.3040 zone awaiting for the US FOMC rate decision. Economists expect no change from 0.25% but the risk may be that if the Fed is more dovish than what the market thinks, then you may see dollar selling in the pipeline. For the rest of London and New York session, we are still waiting for 1.3145 and support at 1.2983.

USD/JPY

USD/JPY reached the highest level since Dec 28 at the time of writing to 78.10 in London time. The headline news was that Japan reported its first annual trade deficit in 30 years raising concerns about its fiscal health. The data also showed Japan's exports declined for the third consecutive month - dropped 8% in Dec from a year earlier. JPY traders no doubt will now monitor if the deficit will continue to rise or if Japan's sovereign rating is in question. Any hint of that should result in shorting the JPY. For the rest of the day and subject to FOMC release expect 77.60 (61.8% fib) to 78.25 trading range.