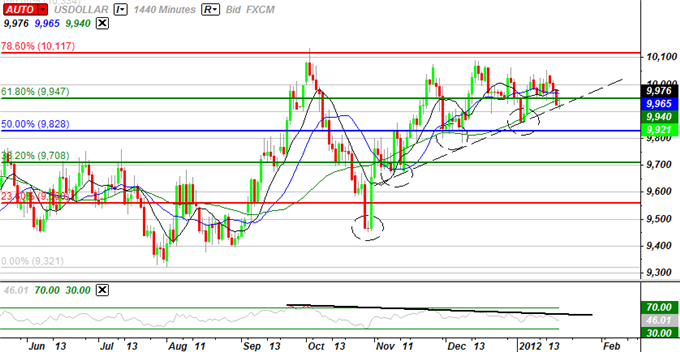

Dollar Slides a Fourth Day as Risk Appetite Persists, Euro Rallies

On the week, the dollar

finds itself significantly lower against all of its major counterparts

with the exception of the Japanese yen. This is a move that fits the

picture that the broader capital market is painting for us. Among the

signs, we find the S&P 500 advancing to fresh five-month highs,

volatility indexes are testing lows not seen since July and the euro is

charging higher across the board. When the masses are pining for

liquidity and safety of funds at the cost of a negative real rate of

return, the greenback will shine. And, conversely, when this sentiment extreme

isn’t pressuring the masses; funds will seek greater diversity. That

said, a move away from an extremophile currency does not necessarily

mean that risk appetite will naturally climb to new heights.

Everything we have seen from

the capital and FX markets suggests that what we have seen to this

point is a pull back or retracement. As the jitters of panic in the

spread of a global crisis pass, there is room to unwind positions that

look to speculation on or insure against impending catastrophe. Traders

must ask: how much premium is there to unwind, and will fear return

before this correction is naturally completed?

Euro Marks a Critical Technical Break Higher as Relief Pours In

After a round of Spanish and

French bond auctions through Thursday’s session, we have officially

closed out the last of this week’s important bond auctions. What started

as a period that was destined for disaster after last Friday’s round of

sovereign ratings downgrades (including France, Italy, Spain and

Portugal), we are ending with a sigh of relief.

Objectively, the rates that the various governments pulled from the

market are not sustainable for financing deficits and spending over the

medium to long-term, but they do ease the threat of imminent doom (a

complete collapse of credit and funding). And, risk of uncontrollable

financial crisis was what drove the shared currency so low, so quickly.

Therefore, it is only reasonable that the immediate pressure relief

should lead to near-term recovery. That said, over-estimating the pace

(and possibly depth) of the crisis doesn’t imply a recovery with higher

yields and non-existent risk.

With the bullish tide that

accompanies this corrective rally, we can see optimism stain bond

auctions outcomes and expectations for various open-ended problems. A

notable example is the negotiations between banks and Greece for a

viable agreement to help Greece to a surplus. FT reported a deal was

close while the New York Time says Hedge Funds may sue. I refer to Fitch

that says: regardless, it would be a default.

British Pound Slow to Follow Euro Higher, Looking Ahead to GDP

The FTSE 100 closed at a

five-month high through Thursday’s close in London, but this is yet

another example of asset pricing running astray of genuine fundamental

potential. Typically, the stock market will follow growth potential

through an ‘investment, wage, spending, production, revenue increase’

cycle. Yet, we know that expansion is exactly the opposite of what’s in

store for the United Kingdom through the immediate future. In fact, the

Bank of England Governor, Chancellor of the Exchequer, World Bank and

industry groups have all warned that the country may dip into period of

negative growth – if not technical recession. Suggestion an economic

slump and all it would entail has already been priced in is preposterous

as it entails an indefinite period of little-to-no dividend income

alongside rising capital loss risk. This raises a very real red flag for

next week’s 4Q GDP reading. Following the euro higher could set the sterling up for a big fall given the correct fundamental winds.

Gold Running at the Same Steady Pace as the S&P 500, With Better Fundamentals

Gold’s advance since the

beginning of this year has run at about the same pace as the S&P

500’s gait: consistent but lacking for momentum. IN fact, looking at an

intraday chart of the metal overlaid with the index; you would see a

remarkable consistency in the two assets’ performance. In fact, the

two-week rolling correlation between the two is currently 0.90

(exceptionally strong). That is very unusual given one is a safe haven

and the other a risk barometer. We could attribute the general

performance to anti-dollar capital flows, but that ignores the underling

drive. Moving away from the greenback is essentially moving away from

cash. In other words, capital is being reinvested into safe and risky

assets.

ECONOMIC DATA

|

GMT

|

Currency

|

Release

|

Survey

|

Previous

|

Comments

|

|

0:30

|

AUD

|

Import price index (QoQ) (4Q)

|

0.6%

|

0.0%

|

Terms of trade important for Australia’s export-dependent economy

|

|

0:30

|

AUD

|

Export price index (QoQ) (4Q)

|

-2.0%

|

4.0%

|

|

|

1:35

|

CNY

|

MNI January Flash Business Sentiment Survey

|

Comes after GDP figures showing slowest growth in more than 2 years

|

||

|

2:30

|

CNY

|

HSBC Flash China Manufacturing PMI (JAN)

|

49

|

||

|

4:30

|

JPY

|

All Industry Activity Index (MoM) (NOV)

|

-0.9%

|

0.8%

|

Could point to period of slow growth in Japanese economy

|

|

7:00

|

EUR

|

Producer Prices (MoM) (DEC)

|

0.1%

|

0.1%

|

Price pressures to ease further amid threat of recession

|

|

7:00

|

EUR

|

Producer Prices (YoY) (DEC)

|

4.6%

|

5.2%

|

|

|

9:30

|

GBP

|

Retail Sales Ex Auto Fuel (MoM) (DEC)

|

0.7%

|

-0.7%

|

Some improvement expected amid holiday season

|

|

9:30

|

GBP

|

Retail Sales Ex Auto Fuel (YoY) (DEC)

|

1.7%

|

0.5%

|

|

|

9:30

|

GBP

|

Retail Sales (MoM) (DEC)

|

0.6%

|

-0.4%

| |

|

9:30

|

GBP

|

Retail Sales (YoY) (DEC)

|

2.4%

|

0.7%

| |

|

12:00

|

CAD

|

Consumer Price Index (MoM) (DEC)

|

-0.2%

|

0.1%

|

Price pressures remain weak in Canada; to further dampen expectations of BoC rate hikes

|

|

12:00

|

CAD

|

Consumer Price Index (YoY) (DEC)

|

2.7%

|

2.9%

|

|

|

12:00

|

CAD

|

Bank Canada CPI Core (MoM) (DEC)

|

-0.2%

|

0.1%

| |

|

12:00

|

CAD

|

Bank Canada CPI Core (YoY) (DEC)

|

2.2%

|

2.1%

| |

|

12:00

|

CAD

|

Consumer Price Index (DEC)

|

120.8

|

120.9

| |

|

13:30

|

CAD

|

Wholesale Sales (MoM) (NOV)

|

0.5%

|

0.9%

| |

|

15:00

|

USD

|

Existing Home Sales (DEC)

|

4.65M

|

4.42M

|

Recovery in US real estate market has lagged behind rest of the economy

|

|

15:00

|

USD

|

Existing Home Sales (MoM) (DEC)

|

5.2%

|

4.0%

|

|

GMT

|

Currency

|

Upcoming Events & Speeches

|

|

1/21

|

EUR

|

EU’s Barroso Speaks in Guimaraes, Portugal

|

SUPPORT AND RESISTANCE LEVELS

|

\Currency

|

EUR/USD

|

GBP/USD

|

USD/JPY

|

USD/CHF

|

USD/CAD

|

AUD/USD

|

NZD/USD

|

EUR/JPY

|

GBP/JPY

|

|

Resist. 3

|

1.3132

|

1.5640

|

77.81

|

0.9442

|

1.0214

|

1.0556

|

0.8136

|

101.34

|

120.84

|

|

Resist. 2

|

1.3090

|

1.5602

|

77.64

|

0.9413

|

1.0191

|

1.0521

|

0.8110

|

101.02

|

120.51

|

|

Resist. 1

|

1.3048

|

1.5565

|

77.48

|

0.9383

|

1.0167

|

1.0487

|

0.8083

|

100.69

|

120.18

|

|

Spot

|

1.2965

|

1.5489

|

77.16

|

0.9323

|

1.0120

|

1.0419

|

0.8031

|

100.04

|

119.52

|

|

Support 1

|

1.2882

|

1.5413

|

76.84

|

0.9263

|

1.0073

|

1.0351

|

0.7979

|

99.39

|

118.85

|

|

Support 2

|

1.2840

|

1.5376

|

76.68

|

0.9233

|

1.0049

|

1.0317

|

0.7952

|

99.06

|

118.52

|

|

Support 3

|

1.2798

|

1.5338

|

76.51

|

0.9204

|

1.0026

|

1.0282

|

0.7926

|

98.74

|

118.19

|