THE TAKEAWAY: [Fed’s Bernanke Testifies Before House] > [Urges Caution in Overly Rapid Deficit Cutting] > [USD Weakens]

Federal Reserve Chairman Ben

Bernanke testified before the House Budget Committee on the U.S.

economic outlook today. The appearance comes just a week after the Fed’s

announcement that it is likely to keep interest rates near zero until

at least late 2014, extending its previous time frame by at least a year

and a half.

At the testimony, Bernanke

began by defended the FOMC’s decision to maintain its highly

accommodative stance of monetary policy and to maintain its program to

extend the average maturity of its securities holdings. Bernanke

reiterated a bearish tone on the U.S. economic recovery, describing the

pace of recovery as “frustratingly slow”, although the Fed is indicating

that expect a somewhat stronger growth this year than in 2011.

Moving onto fiscal policy

challenges, Bernanke warned against overly rapid deficit cutting,

appealing to lawmakers that “even as fiscal policymakers address the

urgent issues of fiscal

sustainability, they should take care not to unnecessarily impede the

current economic recovery. Fortunately, the two goals of achieving

long-term fiscal sustainability and avoiding additional fiscal headwinds

for the current recovery are fully compatible--indeed,

they are mutually reinforcing.” Even after economic conditions have

returned to normal, the Fed cautioned that the nation will still face a

sizable structural budget gap if current budget policies continue. Even

assuming that the economy is close to full employment, the Fed

anticipates that the budget deficit would be more than 4 percent of GDP

in fiscal year 2017.

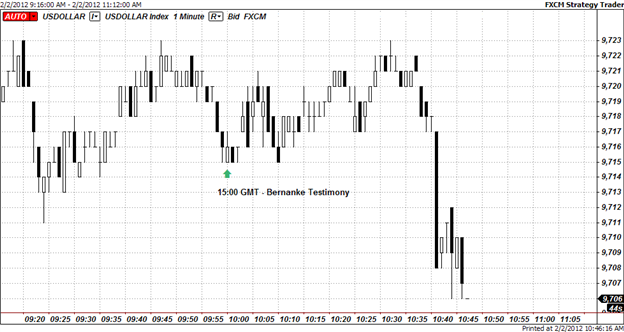

US Dollar 1-minute chart: 2 February 2012

Immediately after the release of Bernanke’s testimony, the U.S. dollar pared back recent losses, with the U.S. Dollar Index (Ticker: USDOLLAR) reaching

9723 before tumbling down towards 9706 at the time of this report. The

U.S. dollar fell against major currencies including the euro, Australian

dollar and Canadian dollar.

The U.S. dollar declined

sharply as the markets viewed the FOMC’s announcement as “dovish”,

allowing a third round of quantitative easing to remain on the table for

some time this year.

In his testimony, Bernanke noted the following outlook on the U.S. economy and fiscal policy challenges:

Having a

large and increasing level of government debt relative to national

income runs the risk of serious economic consequences. Over the longer

term, the current trajectory of federal debt threatens to crowd out

private capital formation and thus reduce productivity growth. To the

extent that increasing debt is financed by borrowing from abroad, a

growing share of our future income would be devoted to interest payments

on foreign-held federal debt. High levels of debt also impair the

ability of policymakers to respond effectively to future economic shocks

and other adverse events.

Even the

prospect of unsustainable deficits has costs, including an increased

possibility of a sudden fiscal crisis. As we have seen in a number of

countries recently, interest rates can soar quickly if investors lose

confidence in the ability of a government to manage its fiscal policy.

Although historical experience and economic theory do not indicate the

exact threshold at which the perceived risks associated with the U.S.

public debt would increase markedly, we can be sure that, without

corrective action, our fiscal trajectory will move the nation ever

closer to that point.

To achieve

economic and financial stability, U.S. fiscal policy must be placed on a

sustainable path that ensures that debt relative to national income is

at least stable or, preferably, declining over time. Attaining this goal

should be a top priority.

Even as

fiscal policymakers address the urgent issue of fiscal sustainability,

they should take care not to unnecessarily impede the current economic

recovery. Fortunately, the two goals of achieving long-term fiscal

sustainability and avoiding additional fiscal headwinds for the current

recovery are fully compatible--indeed, they are mutually reinforcing. On

the one hand, a more robust recovery will lead to lower deficits and

debt in coming years. On the other hand, a plan that clearly and

credibly puts fiscal policy on a path to sustainability could help keep

longer-term interest rates low and improve household and business

confidence, thereby supporting improved economic performance today.

Fiscal

policymakers can also promote stronger economic performance in the

medium term through the careful design of tax policies and spending

programs. To the fullest extent possible, our nation's tax and spending

policies should increase incentives to work and save, encourage

investments in the skills of our workforce, stimulate private capital

formation, promote research and development, and provide necessary

public infrastructure. Although we cannot expect our economy to grow its

way out of our fiscal imbalances, a more productive economy will ease

the tradeoffs that we face and increase the likelihood that we leave a

healthy economy to our children and grandchildren.

No comments:

Post a Comment