The Euro finds itself at a potential crossroads.

Does the single currency zone remain intact and prove that the Euro itself is a viable currency?

Does the single currency zone remain intact and prove that the Euro itself is a viable currency?

Do Germany and other core nations come in

to rescue the periphery despite significant domestic opposition?

As it

stands, recent trends plainly point to continued turmoil and further

Euro losses.

Yet a lot can happen in six months, and it will be crucial

to monitor developments in the Euro Zone in the first half of 2012 and

how it affects the Euro exchange rate.

We foresee Euro declines in the first half of 2012.

How low can we go?

Many factors will affect this, but we expect to see

Euro/Dollar (EUR/USD) to reach at least 1.20 in the next six months, and

perhaps even touch 1.15.

Debt Crisis Front and Center

The current European debt crisis started with

serious doubts over Greek debt as early as 2009, but 2011 marked the

year in which worries over the periphery spilled into the Euro Zone

core. Whereas previous debt problems had been limited to the

comparatively small Greek, Irish, and Portuguese economies, trader

worries transferred into core nations as tensions hit fever pitch.

Investors aggressively sold Italian and Spanish

bonds as they doubted the solvency of governments in the Euro Zone’s

third and fourth-largest economies. Italy, the Euro Zone’s third-largest

economy, has total public debts representing over 120 percent of

domestic Gross Domestic Product. With such an enormous debt load, it is

important to watch the interest rates that Italy must pay on its debt.

If it must pay unsustainably high interest rates – believed to be around

7% for 10-year bonds, which was seen on several days in November and

December – Italy may be pushed beyond the point of “no return”. That is

to say, it will depend on external aid to remain fully solvent.

What could conceivably put Italy on the right path

and stave off a fiscal crisis on a scale few could imagine? The first

step must be a credible plan for Italy to meet its debt

obligations—likely led by strong fiscal austerity and real commitment to

economic reforms to enhance productivity. The new Italian government

has announced measures to cut deficits via increased taxes and reduced

spending. Of course such deficit-cutting measures are complicated by the

fact that the Italian economy remains stuck in a period of extremely

low growth. In the period from 2000 to 2010, Italy held the third-lowest

GDP growth rate in the world behind Haiti and Zimbabwe.

The short-term budget cutting measures that have

been taken thus far have proven insufficient and perhaps even

counterproductive. The entire Euro Zone is now expected to enter a

recession through the first quarter of 2012, and any aggressive spending

cuts and/or tax increases from Spain and Italy could exacerbate the

downturn.

The new conservative government in Spain has

announced fairly aggressive deficit-cutting measures that have been met

with noteworthy improvements in domestic bond prices, and hence lower

interest rates. Yet the spread between 10-year Spanish bond yields and

the benchmark German equivalent continues to trade near its widest

levels since the Euro’s inception. Markets seem more optimistic, but the

overwhelming theme is pessimism over the solvency of key Euro Zone

governments.

The unvarnished truth is that an orderly solution to

Euro Zone fiscal woes seems exceedingly unlikely. Ideally we would see

commitments to real structural changes in regional governance. For

example, markets might be more likely to lend to Italy and Spain if all

Euro Zone nations were prohibited from running budget deficits beyond a

certain level. Such rules have existed for years in the form of the Euro

Zone’s “Growth and Stability Pact”, but the missing link remains the

lack of real consequences for non-compliance. We foresee a continuation

of the trend of patchwork short-term solutions that continue to roil

financial markets. Such initiatives may involve attempts at Italian

fiscal austerity, European Central Bank aid, and/or international aid.

Yet the problems of Euro Zone debt and competitiveness will remain

significant.

As traders, we will look for opportunities to play

ongoing crises through the Euro/Dollar (EUR/USD) exchange rate. Although

shorter-term rallies as high as $1.3500 seem possible, the overall

trend favors further EURUSD weakness.

Medium-term technical studies point to more Euro weakness

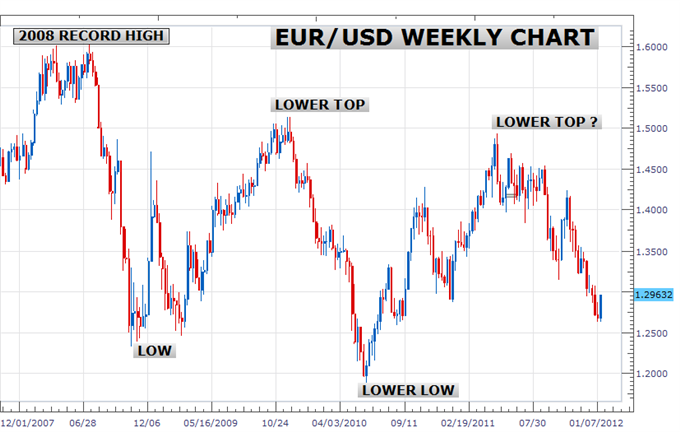

A closer look at the longer-term chart shows the

market locked in a well defined downtrend since posting record highs

just over 1.6000 back in 2008. An initial low was recorded in October

2008 by 1.2330, followed by a lower top at 1.5145 in November 2009, a

lower low at 1.1875 in June 2010 and the latest anticipated lower top by

1.4940 in April 2011. The failure to move higher in 2011 opens the door

for the current downside extension which should ultimately look to

retest and eventually break below the 1.1875, June 2010 lows. This would

confirm the next lower top at 1.4940 and potentially point towards a

deeper drop towards 1.1500.

As such, our outlook for the first half of 2012 is

predominantly bearish while the market adheres to the broader underlying

downtrend, and we would expect to see a move towards 1.1875 at a

minimum before considering the potential for any meaningful recovery. In

the interim, any rallies should therefore continue to be very well

capped, with overbought short-term rallies viewed as compelling

opportunities to look to build on short positions. Ultimately, only a

2-week close back above 1.3500 would bring this outlook into question

and give reason for concern.

No comments:

Post a Comment